blockchain applications & real-world use cases disrupting the status quo

A blockchain database is managed autonomously using a peer-to-peer network and a distributed timestamping server. They are authenticated by mass collaboration powered by collective self-interests. Such a design facilitates robust workflow where participants’ uncertainty regarding data security is marginal. The use of a blockchain removes the characteristic of infinite reproducibility from a digital asset.

Supply Chain Management

The process of understanding and accessing the flow of crypto has been an issue for many cryptocurrencies, crypto-exchanges and banks. The reason for this is accusations of blockchain enabled cryptocurrencies enabling illicit dark market trade of drugs, weapons, money laundering etc. A common belief has been that cryptocurrency is private and untraceable, thus leading many actors to use it for illegal purposes. This is changing and now specialised tech-companies provide blockchain tracking services, making crypto exchanges, law-enforcement and banks more aware of what is happening with crypto funds and fiat crypto exchanges.

The fact that the ledger is distributed across each part of the network helps to facilitate the security of the blockchain. Most cryptocurrencies use blockchain technology to record transactions.

Most blockchains are designed as a decentralized database that functions as a distributed digital ledger. These blockchain ledgers record and store data in blocks, which are organized in a chronological sequence and are linked through cryptographic proofs.

Once recorded, the data in any given block cannot be altered retroactively without alteration of all subsequent blocks, which requires consensus of the network majority. Although blockchain records are not unalterable, blockchains may be considered secure by design and exemplify a distributed computing system with high Byzantine fault tolerance. Decentralized consensus has therefore been claimed with a blockchain.

For new transactions, this means that 51% of the network must be satisfied the verification criteria have been met ie. In the case of Bitcoin, the sender must present a private key, signifying ownership, and a public key, which represents the ‘address’ of the digital wallet the Bitcoin is held in.

Chain

- Earlier this month,Coindeskspotted the patent application that talks about three ways for verifying timestamps with one involving the use of a blockchain platform.

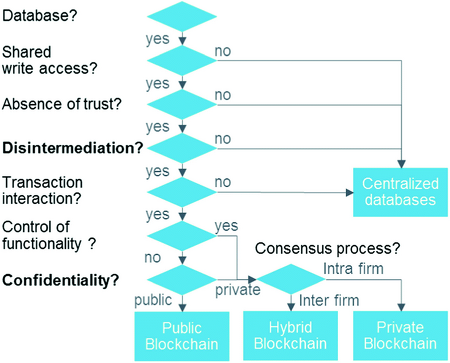

We anticipate a proliferation of private blockchains that serve specific purposes for various industries. As its name implies, a blockchain is a chain of blocks, which are bundles of data that record all completed transactions during a given period. For bitcoin, a new block is generated approximately every 10 minutes. Once a block is finalized or mined, it cannot be altered since a fraudulent version of the public ledger would quickly be spotted and rejected by the network’s users.

For example, the bitcoin network and Ethereum network are both based on blockchain. On 8 May 2018 Facebook confirmed that it would open a new blockchain group which would be headed by David Marcus, who previously was in charge of Messenger. Facebook’s planned cryptocurrency platform, Libra, was formally announced on June 18, 2019. It is “an open, distributed ledger that can record transactions between two parties efficiently and in a verifiable and permanent way”. For use as a distributed ledger, a blockchain is typically managed by a peer-to-peer network collectively adhering to a protocol for inter-node communication and validating new blocks.

Earlier this month,Coindeskspotted the patent application that talks about three ways for verifying timestamps with one involving the use of a blockchain platform. Blockchain, which is gaining in prominence and popularity among all sorts of companies, is a public ledger of all transactions that have ever been executed. It is constantly growing as “completed” blocks are added to it with a new set of recordings.

Much of the initial private blockchain-based development is taking place in the financial services sector, often within small networks of firms, so the coordination requirements are relatively modest. Nasdaq is working with Chain.com, one of many blockchain infrastructure providers, to offer technology for processing and validating financial transactions. The Bank of Canada is testing a digital currency called CAD-coin for interbank transfers.

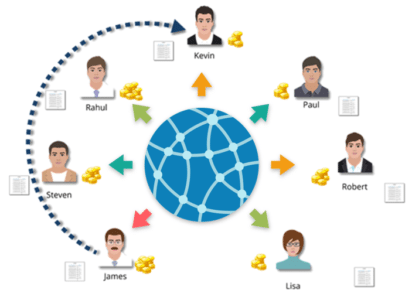

Each node or computer connected to the network receives a copy of the blockchain. This allows the participants to verify and audit transactions independently and relatively inexpensively.

Prominent Blockchain Applications To Know

Cryptocurrencies of all types make use of distributed ledger technology known as blockchain. Blockchains act as decentralized systems for recording and documenting transactions that take place involving a particular digital currency. Put simply, blockchain is a transaction ledger that maintains identical copies across each member computer within a network.

The creation of blockchain technology brought up many advantages in a variety of industries, providing increased security in trustless environments. For instance, when compared to traditional centralized databases, blockchains present limited efficiency and require increased storage capacity. The analysis of public blockchains has become increasingly important with the popularity of bitcoin, Ethereum, litecoin and other cryptocurrencies. A blockchain, if it is public, provides anyone who wants access to observe and analyse the chain data, given one has the know-how.

The development, some argue, has led criminals to prioritise use of new cryptos such as Monero. The question is about public accessibility of blockchain data and the personal privacy of the very same data. The first blockchain was conceptualized by a person (or group of people) known as Satoshi Nakamoto in 2008.

Sources such as Computerworld called the marketing of such blockchains without a proper security model “snake oil”. Blockchain transaction ledgers are also decentralized, which means copies exist on numerous ‘nodes’. Nodes are computers participating in a particular Blockchain application. In the case of public Blockchains such as cryptocurrencies, the number of nodes can reach millions. For a change to be made to a Blockchain, at least 51% of the participating nodes must verify it.

It confirms that each unit of value was transferred only once, solving the long-standing problem of double spending. A blockchain can maintain title rights because, when properly set up to detail the exchange agreement, it provides a record that compels offer and acceptance. Blockchain was invented by a person (or group of people) using the name Satoshi Nakamoto in 2008 to serve as the public transaction ledger of the cryptocurrency bitcoin. The invention of the blockchain for bitcoin made it the first digital currency to solve the double-spending problem without the need of a trusted authority or central server. The bitcoin design has inspired other applications, and blockchains that are readable by the public are widely used by cryptocurrencies.

What are the applications and use cases of Blockchains?

Real-world uses of blockchain, including supply chain monitoring, equity management cross-border payments and election voting.